VEHICLES

-

What to do in the event of a car accident?

In the event of an accident, you must complete a CAFD (Car Accident Friendly Declaration), even if the vehicle has been misled and has not collided with another vehicle, person or object (eg motorway separator). This is because, despite the designation that was given to the document - CAFD - it works as a form in which are summarized, in an objective way, the elements that the Insurers understand as necessary to be able to properly regularize car accidents.

-

How to complete a Car Accident Friendly Declaration?

In the event of an accident, we advise you to complete the Car Accident Friendly Declaration (CAFD) together with the other party.

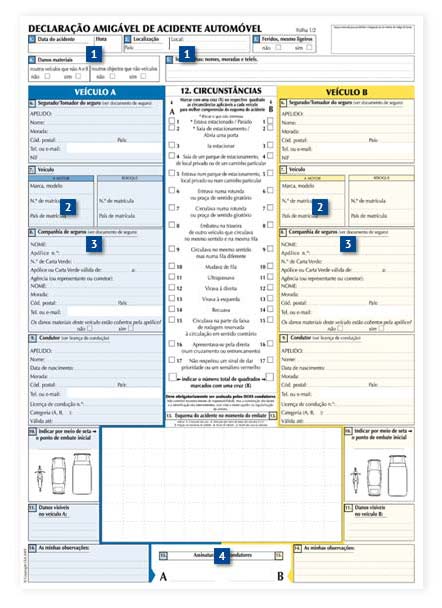

At the accident site, it is essential to fill in (in front of the Friendly Declaration):

1 - Date and location of accident

2 - Registration number of the damaged vehicles

3 - Insurance certificate number of the damaged vehicles

4 - Whenever possible, the signatures of drivers

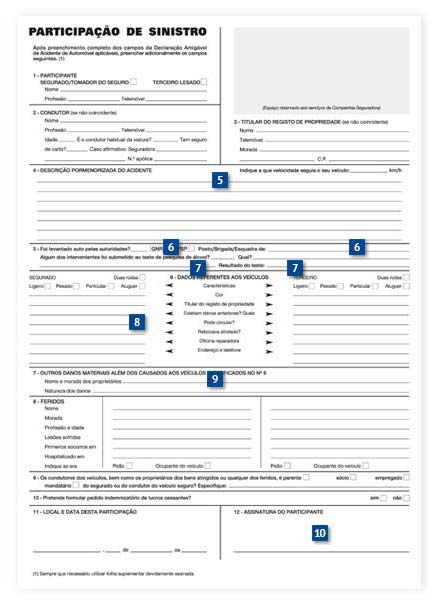

It is important to include the following information to be completed by our Customer/Driver (on the back of the Friendly Declaration):

5 - Detailed description of the accident

6 - Intervention by the authorities and their identification

7 - Alcohol test and the result obtained

8 - If the vehicle was immobilized as a result of the accident

9 - Other damages, in addition to the vehicles involved

10 - Finally the signature of the Policyholder or stamp (in case it is a company)

-

How to proceed in case of a car accident that has occurred in Portugal, with a foreign registration vehicle?

If the insurance of the foreign registration vehicle has been effected in other country, the Automobile Guarantee Fund (FGA) should be contacted which, as the managing office, will indicate the name and address of the Insurer operating in Portugal that will be the foreign Insurer's correspondent.

-

How to proceed, in case of a car accident in Portugal, with a vehicle whose driver does not have a valid insurance?

In this case it is necessary to contact the Automobile Guarantee Fund (FGA), which will be responsible for the payment of compensation to any injured in the following terms:

• Death or personal injury when the person responsible for the accident is unknown, if that person does not benefit from valid or effective insurance or the insurer has been declared bankrupt.

• Material damages when the person responsible for the accident, being known, does not benefit from valid or effective insurance.

• In the case of material damages there is an amount of € 299.28 to be deducted from the compensation provided by the FGA.

This Fund is managed by the Insurance and Pension Funds Supervisory Authority (ASF) and fed by a percentage of the Automobile Insurance premium.

-

What is the IDS Convention?

The Insured Direct Indemnity Convention (IDS) was signed by almost all Insurers operating in the Portuguese Market and aims to accelerate the Settlement of Automobile Claims, allowing each insured to go to his own Insurer even when he is not responsible for the occurrence.

The operation of this Convention presupposes those cases in which there is:

• Collision between two vehicles with Portuguese registration;

• That the damages are only material (there can be no personal injury);

• That the damages of the non-responsible driver do not exceed € 4,987.97;

• That both vehicles must be insured in two different Insurers and both Insurers must have signed the Convention;

• That the completion of the DAAA is correct, particularly with regard to the ACCIDENT CIRCUMSTANCES.

-

Is it possible to insure all risks in the Car Insurance?

The answer is no, that is, in addition to the Civil Liability coverage, which is legally imposed and regulated, other coverage can be contracted, at the Insured's request, called "Own Damage" such as shock, collision and rollover or theft and other damages that the vehicle itself may suffer. These special safeguards are vulgarly, yet wrongly referred as "all risks".

-

I had a car accident with a third-party vehicle whose driver had blood alcohol and is responsible for what happened. Who will indemnify the repair of my car?

Under the Uniform Compulsory Motor Civil Liability Insurance Policy law, issued by the Insurance and Pension Funds Supervisory Authority (ASF), the fact that a driver, responsible for the occurrence of an automobile accident, has been driving under the effect of alcohol, does not exonerate his insurer to indemnify the third party not responsible, so that the expert's report must be checked with the Insurer of the responsible driver and the repair must be paid by the same.

-

What is CIMASA?

As the acronym in its name indicates, the Insurance Information, Mediation, Ombudsman and Arbitration Centre can be used to resolve all disputes arising from the formation, execution and termination of insurance contracts.

The Arbitrator's decision is equivalent to a court judgement, but is handed down in a shorter space of time, making the process simpler, more informal and less bureaucratic.

-

When is there an increase to the car insurance premium?

Under the Uniform Compulsory Motor Civil Liability Insurance Policy law, issued by the Insurance and Pension Funds Supervisory Authority (ASF), there is an increase of the Automobile Insurance Premium when there have been claims that have given rise to the payment of indemnities by the Insurer, or the creation of a provision, and in the latter case, it is not enough that the Insurer has constituted the provision for the increase to occur, being also necessary that the Insurer has assumed responsibility before third parties.

In other words, in situations where, for example, the insured vehicle is damaged by an unknown vehicle, whose registration no one has seen and the Insurer pays for the repair of the insured vehicle, there will be a rise in the premium of the policy.

ACCIDENTS AT WORK

-

Is it mandatory contracting an Accident at Work Insurance for all personnel at my service?

Employers are obliged to transfer responsibility for repairing the damages arising from an accident at work provided for in the Law, to entities authorized to carry out this insurance.

-

And, in the case of Independent Workers, is there also such a requirement?

Independent Workers, those who are self-employed, are obliged to carry out an Accident at Work Insurance that guarantees the same benefits provided for in the Law for workers on behalf of others.

-

Should the remuneration to be transferred be limited to the basic remuneration?

The amount of the remuneration to be transferred to the insurer shall comprise the basic remuneration and all other supplementary or additional benefits made in cash or in kind.

-

What can these supplementary benefits be?

The supplementary benefits are all those that, due to their regularity of payment, become part of the concept of retribution. Examples include, among other things, assiduity and productivity premiums, sales commissions, allowances for working hours exemption, meals, isolation or shift, as well as Christmas and holiday bonuses, which, by their generalization and mandatory nature, are already part of the mentioned retribution.

-

What are benefits in kind?

Benefits in kind are all those that, although not paid in cash, do not fail to integrate the concept of retribution, provided that there is regularity in their attribution. Mention should be made, for example, of the meals distributed to the worker in lieu of the food allowance and the fish trunks assigned to the fisherman after work.

For purposes of inclusion in the salary to be transferred, it is necessary to convert the value of these benefits into cash.

-

What are the consequences of insufficient insured retribution?

In the case where the remuneration declared for the purpose of the insurance premium is less than the actual remuneration, the insurance entity shall be liable only in respect of that remuneration. In this case, the employer will be responsible for the difference in compensation and pensions and, proportionally, for the expenses and allowances provided for in the Law.

-

How to proceed in the event of personnel traveling to missions abroad?

The insurer must be informed in advance about the travel abroad of insured workers, provided that their stay is longer than 15 days.

It should be noted that, regardless of the period of travel, in case of an accident occurring in foreign territory, the insurer will only be responsible for the costs of treatment, transportation and repatriation, if this is expressly stated in the Particular Conditions of the Policy.

-

Does the Accident at Work Insurance policy provide coverage for accidents that occur during the journey from home to work and vice versa?

As this risk is part of the legal concept of work accident, the uniform policy created in line with the legislation in force contemplates this type of accident, without the need to request a separate coverage.

-

How should I proceed in case of an accident?

Employers or those who represent them in the direction or supervision of work shall ensure the immediate and indispensable medical assistance to the victim, as well as the most adequate transportation for that purpose. Within 24 hours the claim participation must be completed and sent to the insurer or APS (Associação Portuguesa de Seguradores).

-

How to proceed in the event of an accident resulting in death or leading to the death of the victim?

As soon as this fact is known, the employer must immediately notify the insurer of this situation, without prejudice to sending the claim participation within the prescribed time limit.

-

What responsibilities can be attributed to me if there is a claim for non-compliance with the rules on Safety, Hygiene and Health at work?

In these cases, the insurer will take over the entire management of the process, with clinical follow-up and payment of all expenses/disabilities for the injured party.

At the end of the process, it will pursue the right of recourse with the employer.

+351 217 220 100

+351 217 220 100